The Zelle Business Model: How does Zelle make money?

Are you curious about how does Zelle make money? Zelle is an instant-payments network that has made it possible to send and receive money in seconds. It is a convenient and secure way to send money from person to person. No more dealing with checks, cash, or other outdated methods of monetary exchange!

The registration process only takes minutes, and you can download the free Zelle app on your mobile device instantly after signing up. You don’t need any information about the recipient–just their email address or phone number where they will receive automatic notifications when funds are sent to them.

Zelle: Network Profile

Let’s look in depth at how Zelle works and how does Zelle make money.

How does Zelle work?

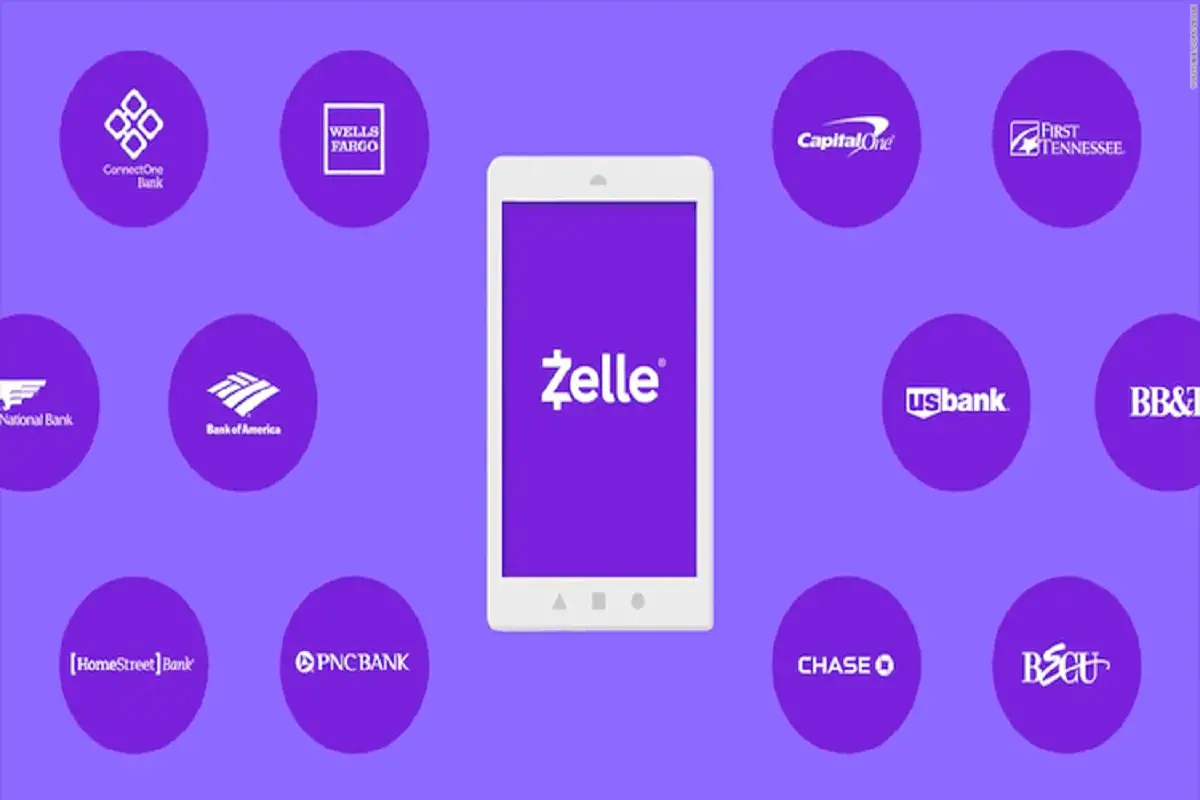

Zelle is a U.S. based digital payments network that is owned by Early Warning Services, LLC, which is a private financial services company owned by the banks JPMorgan Chase, BB&T, Bank of America, Capital One, PNC Bank, U.S. Bank and Wells Fargo. It is a digital payment app that allows U.S. account holders to send money from their bank accounts in just three easy steps!

First, register for the service through Zelle or your partner bank’s mobile application and enter your personal information such as name, birth date, phone number, and Social Security Number into an encrypted form on the banking site. Second, open up the app with access to either one of the banking sites. Third, log in by entering username/password OR Touch ID if available; select “Send” > Choose recipient> Enter Amount> Tap Send Money

Users can transfer funds by providing the recipient’s email address or phone number within minutes of initiating the transaction. The Zelle Network is powered by Mastercard Send and Visa Direct payment rails used extensively across banks as their payments processor, so any bank could join on if they wanted!

Banks that work with Zelle

Zelle is an app that works with 924 financial institutions. Most partners have integrated Zelle into their mobile apps – all you need to send money are a Mastercard or Visa debit or credit card.

The story of Zelle

When Bank of America, Wells Fargo, and JPMorgan Chase realized they were not going to be able to compete on other payment platforms like PayPal and Venmo alone, they established ClearXchange (now known as “Zelle”) in 2011.

ClearXchange was a clunky and slow way to transfer money, with 5-day wait times. It only worked through the website or an app from partner banks—a few of which were nationwide, preventing adoption across the country. The service also had features that varied widely among all their partners’ variations on it—another reason for confusion when trying out clearXchange.

Zelle was launched in September 2017 with more than 30 banks, equal to almost 100 million account holders. This changed everything for the service, which had previously been owned by Bank of America, JPMorgan Chase, and Wells Fargo but sold to Early Warning Services (which itself is owned by a consortium of banks). The speed of product development finally became on par with expectations under Early Warnings’ guidance as they completed Zelle’s launch.

Zelle gained popularity quickly. The consortium of banks put $1 million into TV ads to introduce the app and made it easier for users by standardizing an in-app experience across all participating banks. Gen Xers and Baby Boomers proved to be one of Zelle’s major growth channels when many traditional bank customers chose not to change over from their current provider due to unfamiliarity with newer services. With some big U.S. Banks behind it, there was no stopping Zelle!

Zelle had a quick rise to success and became the first P2P service of its kind in America. The company was able to pave its way into people’s lives, especially those struggling with hyperinflation, because they found that Zelle is an easy alternative for sending money abroad or paying bills without needing traditional bank accounts.

The service, Zelle, has experienced some backlash from other users. This is because many have been scammed by fraudulent users who would sell products or services and then take the money back once they had it in their account without providing what was promised to them. People are now urging people not to use this app for any transaction unless they know who they’re sending funds to since fraudsters can quickly turn around scamming victims again using Zelle’s system with ease!

The idea behind a new payment method like Zelle seems perfect on paper- everyone could conveniently transfer cash digitally no matter where they were at as long as there was cell phone reception. Still, unfortunately, that isn’t really how things work out when putting it into practice.

Zelle has been heavily used in recent years. With 1.2 billion transactions and $307 million, the platform had its upsides despite some hiccups with scams or frauds on their site or mobile app – someone close to you can be scammed just as easily!

How does Zelle make money?

Zelle does not make any money today; it relies exclusively on fees from participating banks such as JP Morgan Chase Bank NA, Citigroup Inc., Wells Fargo & Co., The Bancorp PLC (PNC), TD Ameritrade Holding Corporation (AMTD), which brings up an interesting topic: what happens when Zelle starts making money? Will they have pressure to increase transaction prices for users constantly?

Right now, Zelle is a free service that helps you send money to other people. Participating banks like JPMorgan Chase, Wells Fargo, and Bank of America offer Zelle as an alternative way for their customers to make payments between each other in person or online. Chime recently announced they would be rolling out features similar to those offered by Venmo.

However, unlike the latter’s free-to-use model, which has been very successful since its inception in 2009 (and still going strong), there are no signs yet indicating how much it would cost users who want access these feature from Chime when they become available – potentially making them less attractive than Venmo given the lack of any price difference!

Final Thoughts

Zelle has been in the news for a long time now, but it’s doing more than just sending money. Zelle is also helping small businesses get paid by customers with ease and convenience on their phones. It may be safe to say that this will change how we do business forever!

Other Business Models: Discord, Afterpay, Zoom, Craigslist, Nerdwallet, OfferUp, Honey, Venmo, Carvana, DoorDash, Webull, Hinge, Bumble, Vinted